Introduction

The Third Anti-Tax Avoidance Directive (ATAD 3 or unshell directive) which sets rules to prevent the abuse of shell companies for tax purposes is now with the European Council for further commentary

ATAD 3 applies to EU tax resident undertakings engaged in an economic activity regardless of their legal form – the European Commission announced in 2022 that a similar initiative for non-EU shell companies is underway.

While the Proposed Directive was published by the European Commission in late 2021, during 2023 non-binding amendments by the European Parliament have been proposed which are still under discussion by the EU Member States.

The final version will need to be unanimously approved by all Member States before it can be adopted. The effective date of 1st January 2024 has not changed despite ongoing negotiations on the contents. When adopted, there will be a two-year reference period (i.e.: 1st January 2022 – 31st December 2023). Therefore, the entities operating legitimately right now could already be inadvertently coming within the scope of the draft Directive when/if it is implemented in 2024.

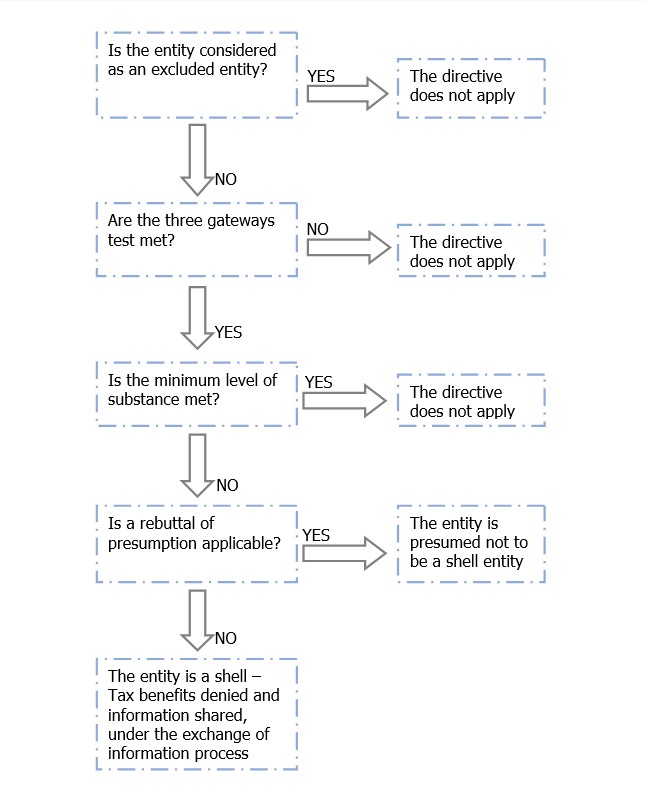

Excluded entities

ATAD 3 is not applicable to certain entities which are excluded from the scope by carve-outs. Excluded entities include certain listed companies, certain regulated financial companies and certain holding companies. The latter in brief concern those holding shares in an operational entity resident in the same Member State as its beneficial owners and those holding companies that are resident in the same Member State as its shareholder(s) or ultimate parent company.

The exemption for entities that have at least five own full-time employees or members of staff that are solely involved in carrying out activities that generate the relevant income has been removed in the 2023 non-binding amended version of ATAD 3.

“Gateway” indicators and “Minimum substance test”

The draft guidance outlines “gateway” indicators that help determine whether a company is at risk of being considered a shell company.

If these indicators are met cumulatively, the company is considered at risk and is subject to further reporting to determine if it meets the “minimum substance” requirements.

- Passive income: more than 65% (instead of 75% provided in the Proposed Directive) of its revenues in the previous two years consists of relevant income.

Relevant income primarily consists of passive income such as interest, dividends, royalties, other income generated from financial assets (including crypto assets), income from financial leasing, immovable and some moveable property

The test is also met if more than 75% of the total book value of the assets of the undertaking consist of immovable property or if the entity holds assets that generate income as dividends and income from the disposal of shares, and the book value of these assets is more than 55% of the total book value of the entity’s assets;

- Cross Border Activity: more than 55% of the book value (instead of 60% provided in the Proposed Directive) of immoveable property and other valuable private property as specifically identified is held outside the Member State in the previous two years or at least 55%, (instead of 60% provided in the Proposed Directive) of relevant income earned is from cross border transactions;

- Management and administration outsourced: decision making on significant functions and administration of its day-to-day operations is outsourced to a third party in the preceding two years (third-party outsourcing is the non-binding recommendation of the EU Parliament clarifying in effect that in house outsourcing is allowed).

The entity which is classified as being at risk, must then indicate through an annual declaration whether it meets the following “minimum substance” indicators:

- Whether the entity has an office space exclusively used or shared with other group entities, (owned or rented), through which it exercises its activities; and

- Whether the entity has an active EU bank account or e-money account within EU through which its relevant income is received; and

- Whether at least one director is resident close to the entity and dedicated to its activities, authorised to take decisions or; a sufficient number of the entity’s employees that are engaged with its core income-generating activities are habitually resident close to the undertaking

If the company does not meet these indicators, it would be treated as a shell company for ATAD 3 purposes.

Rebuttal of presumption of minimum substance

It is expected that additional supporting information can be submitted in respect of its business rationale, employees and decision-making in order to allow an entity to rebut a presumption that it does not have minimum substance.

Rebuttal of presumption of shell undertaking

The undertaking that falls within the above criteria and is presumed to be a shell undertaking, can

- provide extra evidence that it performs a genuine economic activity and has enough connection with the Member State it claims to be a tax resident of

- evidence of the absence of tax benefit in comparing the tax liability of the structure in the group to which it belongs, with and without the interposition of the presumed shell

Tax consequences when a company is considered a shell entity

If an entity qualifies as a shell entity, it shall face several consequences which in effect will aim to neutralise the shell entity’s tax impact, such as disallowing any tax advantages that have been (or could be) obtained through the entity in accordance with double tax treaties and/ or EU Directives.

Specifically, the EU Member State of the shell entity shall refuse any request for the issue of a tax residency certificate for use outside its jurisdiction.

This will ensure that the shell entity shall not be eligible for the tax benefits of the network of double tax treaties of its Member State of residence, or for the application of relevant EU Directives. Despite this, the shell entity will continue to be resident for tax purposes in the respective Member State and will have to continue fulfilling its relevant tax obligations.

In case where the shell entity’s shareholders are tax resident in a EU Member State, then that Member State shall have the right to tax the relevant income of the shell entity in accordance with its national law, as if it had accrued directly to the shareholders.

Moreover, any relevant income of a shell entity which is sourced in an EU country will be subject to withholding tax (where applicable) in that country, disregarding any exemptions afforded by double tax treaties or EU Directives.

Also, ATAD 3 provides for automatic exchange of certain information between EU Member States by amending the Directive on Administrative Cooperation in Direct Taxation. It will also be possible for EU Member States to request another EU Member State to audit specific entities.

Penalties for non-compliance

Failure to comply with the reporting obligation, a minimum penalty a fine of at least 2% of the revenue of the entity is imposed.

The EU Parliament added that in case of a false declaration in the tax return, an additional penalty of at least 4% of the entity’s revenue would be due.

For any further clarifications you may require, please do not hesitate to contact

Gabriel Ioannou Andri Andreou

g.ioannou@ith.com.cy a.andreou@ith.com.cy

+357 22050530 +357 22050626